Award-winning PDF software

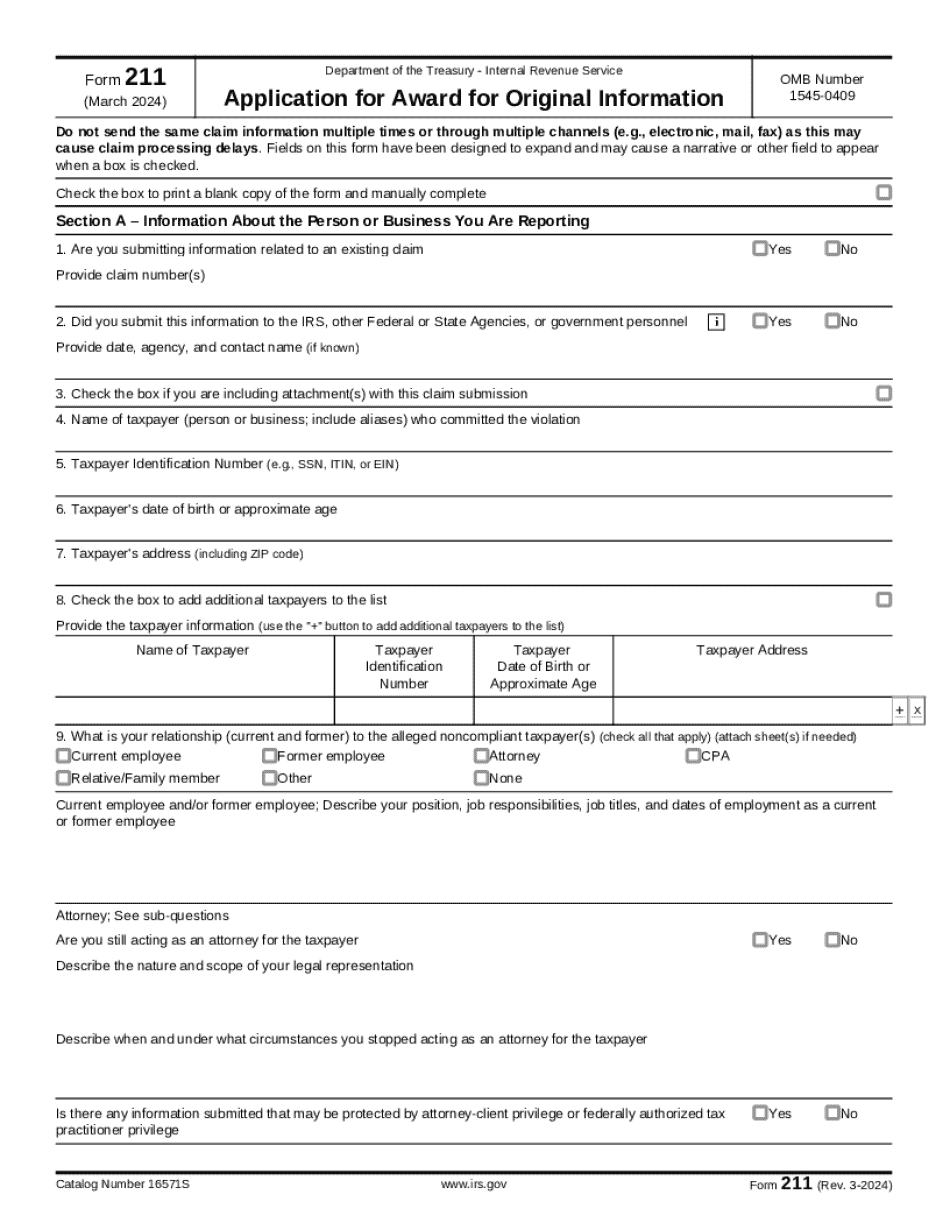

Form 211: application for award for original information

Form 211 is not used to prosecute tax scofflaws. It allows the Bureau of Internal Revenue to investigate those who engage in illegal tax evasion for the purpose of collecting unpaid tax, in order to recover funds that otherwise would be lost to society. The IRS Form 211 award is made for the informant and only for the informant. The award is not returned to the IRS. To be eligible for the IRS Form 211 award, the person must: be employed in a bona fide capacity at the Bureau of Internal Revenue; be employed for a period of more than five years, either part or full time, by the Bureau during the period ending on the date that the notice is submitted; have reported the relevant facts contained in the information required under subsection (2); have been employed by the Bureau and have not been dismissed or discharged for misconduct; be of good character—by reference to.

Tax whistleblower — the dos and don'ts of filing a form 211

The Form 211 is a very, very short, and straight forward form. Anyone can file it and have it go into the trash can. The IRS has no record. However, even if the Form 211 is successful, the IRS is not going to spend your money to pursue a case against a third party. A person that has been investigated for failing to pay taxes may find that the IRS is not interested in pursuing them for failing to pay taxes and that they will have difficulty obtaining one of those IRS funded tax debt relief programs. It is highly probable that when an individual or business fails to pay taxes they will be investigated and prosecuted by the IRS. The IRS is not going to be out there trying to chase down every dollar that they have in collection accounts. The Form 211 and the.

Form 211 - - otc markets

See “Quotations, Service, the National Quotation Bureau.” . Report to the Board. Complete this form to submit quotations to the Board in response to orders from the Board. . Quotation for Sale. Complete this form to sell quotations. See also “Sale, Sales, or Exchanges of Quotations.” . Special Notice Regarding Quotation Processing Time and Prices. Complete this form if this Notice is due to you when you initiate quotations. . Temporary Suspension of Quotations. Complete this form to ask the National Quotation Bureau, in response to orders, to suspend quotations for a short time. See also “Periodical Suspension of Quotations.” . Temporary Imposition of Price Controls. Complete this form to impose price controls for quotation processing time and prices (see “Price Control Suspension.”) Form 212. Suspension Order Procedure. Complete this form to request an order regarding suspension of quotations. See also “Suspension of Quotations. Form 213. Suspension.

Form 211 market maker payments - going public lawyers

The form lists four different ways in which the member can determine which . . The first is the most important : The . Member must identify any market making entity with which the Member has any substantial beneficial interest. To be clear, : “Substantial Beneficial Interest” is defined as the Member's interest in or control of the market maker or a firm on substantially all of its assets or its economic interests that, in itself, have the ability to materially impact the conduct of the market maker. Market making is defined as the creation of a market for a security, whether directly or indirectly. The second is where things get interesting… The form provides a mechanism which might be used in a market maker/ broker-dealer proceeding to establish a direct financial interest. In other words, you might be able to prove that you are the only person with actual legal control over a market maker.

Filing form 211 | filing whistleblower forms - price

As you know, most employees are not interested in filing Form 211 or going to Utah. Many of the employees and contractors with the IRS are only interested in suing the IRS for not paying wages or illegally collecting Social Security or Medicare tax. If an employee or contractor has questions regarding the IRS Form 211, they should contact their office directly. In addition, if a whistleblower is interested in filing the necessary Form 843, the whistleblower employee has the ability to use as a resource. An address is available if the whistleblower has any IRS-related questions. When you file Form 211, the whistleblower and his or her attorney or attorney's agent must file Form 843 with the Treasury Inspector General for Tax Administration (TI GTA) after the whistleblower has filed his or her Form 211. The form states that they are reporting the information to the DOJ. The form.